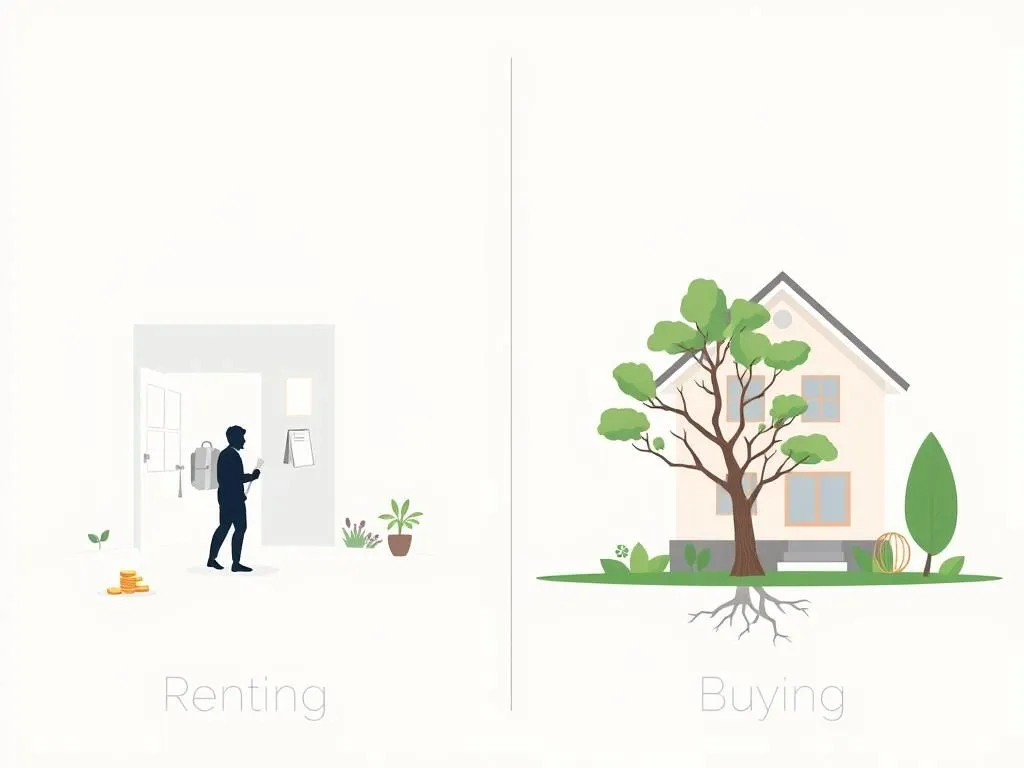

Renting vs Buying: Unraveling the Great Malaysian Property Puzzle

Key Takeaways

- Financial Journey: The choice between renting and buying property in Malaysia is a significant financial journey, particularly for young professionals.

- Diverse Perspectives: There is no universal answer, as the decision involves complex financial factors, lifestyle preferences, and long-term aspirations.

- Informed Decision: Key considerations include personal financial health, career stability, future family plans, and understanding hidden costs, alongside market trends.

The Malaysian Dilemma: Exploring the Core Questions

The echoes of a perennial question reverberate through the bustling streets and quiet neighbourhoods of Malaysia: Is it better to be a tenant or a homeowner? The choice between Renting vs Buying a property isn't just about finding a roof over your head; it's a significant financial journey, particularly for young professionals eager to build their future. This isn't a simple "yes" or "no" answer. It's a complex puzzle with many pieces, each one representing a financial factor, a lifestyle preference, or a long-term aspiration.

For many Malaysians, especially those charting their professional course and envisioning their future, this decision ranks among the most crucial financial considerations. We’re about to embark on an an exciting exploration, peeling back the layers of this dilemma to reveal the diverse perspectives and analyses that can guide your path. Get ready to dive into the financial calculations, lifestyle considerations, and future goals that will help you understand what's truly right for you.

When it comes to property, Malaysia offers a dynamic landscape, and navigating it requires careful thought. Many credible voices are weighing in on this very topic. The Employees Provident Fund (KWSP), a pillar of financial security for Malaysians, wisely suggests asking "5 Questions to Help You Decide" when evaluating the rent vs. buy scenario in Malaysia. These questions highlight the immense importance of considering your individual circumstances before making any big moves. Their insights can guide your path forward1.

Similarly, the experts at Hartamas Real Estate Group also offer valuable perspectives. Their advice prompts individuals to carefully weigh their options, considering both the immediate and long-term implications of each choice. It’s clear that a snap decision simply won't do; thoughtful evaluation is key2.

To help illustrate some of these crucial factors, KWSP provides a clear visual comparison that simplifies the decision-making process. This infographic offers a snapshot of what goes into choosing between renting and buying a home.

A visual comparison of factors to consider when deciding whether to buy or rent a house in Malaysia.

As you can see, both financial bodies emphasize that there’s no universal answer. Your personal financial health, your career stability, and even your future family plans all play a significant role in determining the best path forward.

Beyond the Basics: Deeper Dives into Property Choices

Sometimes, the property journey takes an interesting turn. Have you ever wondered about buying a property and then immediately renting it out? This specific scenario is a hot topic among property investors in Malaysia. A discussion in a Facebook group dedicated to Malaysian property investment tackled this very question. This shows that for some, property isn't just about personal dwelling, but also about strategic investment and generating passive income3. This approach adds another layer of complexity, transforming the simple "rent vs buy for living" into a more intricate "rent vs buy for investment."

The core question, however, often boils down to a straightforward comparison: "Rent or Buy a House in Malaysia: Which is Better?". This question forms the bedrock of countless personal finance debates and articles, reflecting the widespread desire for clarity on such a significant life decision4. It’s a debate that isn’t confined to expert analyses; it spills over into everyday conversations and online communities. Online forums, like the Malaysian Personal Finance subreddit, are buzzing with discussions on this very topic, demonstrating how individuals are actively seeking advice and sharing their experiences to navigate this complex financial landscape5. These discussions often reveal the nuanced perspectives of real people facing real financial choices.

The Surprising Math: Condos and Beyond

When we talk about specific property types, the numbers can get even more interesting. Timothy Tiah, a well-known figure, grabbed attention with his LinkedIn post, delving into the "surprising math" behind the rent vs. buy decision, particularly when it comes to condos in Malaysia6. He also shared accompanying Instagram content, revealing that what many people assume about homeownership might not always be the full picture, especially when you factor in all the hidden costs and potential returns7. His insights challenge conventional wisdom and encourage a deeper look at the actual financial outlay versus the perceived benefits of owning a condo.

What exactly is this "surprising math"? It often involves looking beyond just the monthly mortgage payment versus rent. It means factoring in things like:

- Down Payment: A hefty upfront cost for buying, which renters don't face.

- Interest: Over a 30-year loan, the total interest paid can be staggering.

- Maintenance Fees: Condos often come with significant monthly fees for common areas, security, and facilities.

- Property Taxes: Annual taxes that add to the cost of ownership.

- Insurance: House owner's insurance is a must for buyers.

- Opportunity Cost: The money spent on a down payment and other buying costs could have been invested elsewhere, potentially earning returns.

Timothy Tiah's analysis likely explores how, when all these factors are combined, the total cost of owning a condo might sometimes outweigh the cost of renting, especially in certain market conditions or for specific durations. This is particularly relevant for young professionals who might have limited savings and who value flexibility.

Speaking of young professionals, their perceptions on homeownership versus renting are a critical area of study. A publication on ResearchGate specifically examined "Perceptions Of Young Professional In Malaysia Homeownership Or Renting." This research sheds light on what motivates younger generations: is it the dream of owning a home, or the practical flexibility and lower upfront costs of renting? Their findings are crucial for understanding the evolving dynamics of the Malaysian property market and how economic shifts and lifestyle aspirations are shaping housing choices among the workforce8. Understanding these perceptions helps policymakers and individuals alike better gauge the future trends in the property landscape.

Is It Just About Houses? The Wider "Rent vs. Buy" Principle

The "rent vs. buy" decision isn't unique to homes. It's a fundamental principle that applies to various aspects of life and business, showing just how universal this financial dilemma is. Think about businesses making big purchases. For example, HP, the technology giant, even discusses this principle in the context of acquiring equipment. Their article, "Large Format Printer for Rent or Buy in Malaysia: Decision-Making ...", explores the factors a business considers when deciding whether to rent or buy a large format plotter. This demonstrates that the core financial and strategic questions – upfront costs, long-term commitment, maintenance, and flexibility – are relevant even beyond residential property9.

And to make these kinds of decisions easier, financial tools are readily available. Fidelity, a well-known investment company, offers a general "Rent Vs. Buy" calculator. These calculators are designed to help individuals plug in their own numbers – rent, mortgage, down payment, expected appreciation, and more – to get a clearer picture of which option might be more financially beneficial for them over time10. While not specific to Malaysia, the underlying principles it uses are universally applicable, making it a valuable tool for personal financial planning.

These examples highlight that the Renting vs Buying conundrum isn't merely about a roof; it's a profound financial framework that impacts individuals and businesses across the board. The lessons learned from analyzing property can often be applied to other major financial choices in life.

Key Factors to Weigh When Renting vs Buying

Now that we’ve explored the various facets and expert opinions, let’s consolidate the critical factors you need to weigh when making your own Renting vs Buying decision in Malaysia. This isn't just about comparing monthly payments; it’s about understanding the whole picture.

Financial Considerations: Beyond the Monthly Bill

This is often where the decision-making process begins, but it’s vital to look beyond just the surface.

For Buying:

- Down Payment: This is your initial, often substantial, cash outlay. It can be anywhere from 10% to 20% of the property's price. For a RM500,000 property, that's RM50,000 to RM100,000 upfront. This money is tied up immediately.

- Mortgage Payments: These are your monthly loan repayments, which typically include both principal (the money you borrowed) and interest. Over a 20 or 30-year period, the total interest paid can often equal or even exceed the original loan amount.

- Hidden Costs of Ownership: This is where many people get surprised.

- Maintenance Fees: For apartments and condos, these cover common area upkeep, security, and facilities. They can be hundreds of Ringgit monthly.

- Property Taxes (Quit Rent & Assessment Rates): These are annual taxes paid to the state and local governments.

- Insurance: Fire insurance is mandatory for mortgage, and many opt for comprehensive home insurance.

- Upkeep and Repairs: As a homeowner, you're responsible for everything from a leaky faucet to a broken air conditioner or roof repairs. These can be unexpected and costly.

- Renovation Costs: You'll want to personalize your space, and renovations can quickly add up.

- Legal Fees and Stamp Duty: When buying, there are significant one-off costs for legal services and stamp duty on the sale and purchase agreement and loan agreement. These can amount to several percentage points of the property value.

- Property Appreciation: The hope is that your property's value will increase over time, allowing you to build equity and potentially sell it for a profit later. However, appreciation is not guaranteed and depends heavily on market conditions, location, and economic growth.

- Opportunity Cost of Capital: The money you put into a down payment and other buying costs could have been invested elsewhere, perhaps in stocks, bonds, or other ventures. The potential returns you miss out on by tying up your capital in a property is an important, though often overlooked, financial consideration.

For Renting:

- Monthly Rent: Your primary, predictable housing expense.

- Security Deposit: An upfront cost, usually 2-3 months' rent, which is typically refundable at the end of your tenancy, provided no damage.

- Utility Bills: You pay for your own electricity, water, internet, and sometimes gas.

- No Maintenance Costs: Your landlord is generally responsible for major repairs and maintenance. This means fewer unexpected financial shocks.

- Flexibility with Savings: With lower upfront costs, you have more capital available to save, invest, or use for other life goals.

- No Property Appreciation/Depreciation: You don't benefit if property values go up, but you also don't lose money if they go down.

- Inflation: Rent prices can increase over time, especially when renewing contracts.

Lifestyle & Flexibility: What Kind of Life Do You Want?

Your daily life and future plans play a massive role in this decision.

For Buying:

- Stability and Roots: Owning a home provides a sense of permanence and belonging. It's a place you can truly call your own, decorate as you please, and settle into.

- Customization: Want to paint the walls purple? Build a deck? Install a smart home system? As an owner, you have the freedom to customize your space to your heart's content (within local regulations).

- Community Engagement: Homeowners often feel more invested in their local community, potentially leading to deeper connections and engagement.

- Less Mobility: Buying property means a long-term commitment. If your job requires frequent relocation, or if you simply crave change, selling a house can be a lengthy, costly, and stressful process.

For Renting:

- High Mobility: Renting offers incredible flexibility. You can move for a new job, a change of scenery, or better amenities with relative ease once your lease is up.

- Fewer Responsibilities: You're not burdened with the responsibilities of property maintenance, repairs, or property taxes. This frees up your time and energy.

- Access to Prime Locations: Renting can sometimes allow you to live in desirable, high-cost areas that would be unaffordable to buy in, bringing you closer to work, entertainment, or specific schools.

- Predictable Expenses: Your monthly rent is largely fixed (until lease renewal), making budgeting simpler compared to the unpredictable costs of homeownership.

- No Equity Building: You're not building equity or ownership in the property. Your rent payments essentially pay for a service – the right to live there – without contributing to your net worth in real estate.

Long-Term Goals: Building Wealth and Security

Think about where you want to be in 5, 10, or even 20 years.

For Buying:

- Wealth Building: For many, homeownership is a significant path to building wealth over the long term, especially if property values appreciate. As you pay down your mortgage, you build equity.

- Financial Stability (eventually): Once your mortgage is paid off, your housing costs become significantly lower (just taxes, insurance, and maintenance), providing greater financial freedom in retirement.

- Legacy: A home can be an asset passed down to future generations.

- Forced Savings: Mortgage payments act as a form of forced savings, as a portion goes towards the principal, increasing your equity.

For Renting:

- Investment Flexibility: The money saved from not making a down payment or covering ownership costs can be invested in other assets (stocks, unit trusts, businesses). If these investments perform well, they could potentially outperform property appreciation, especially with the "surprising math" involved in some property markets.

- Lower Risk: Renting shields you from downturns in the property market or unexpected, large home repair bills.

- Focus on Other Goals: Without the demands of homeownership, you might have more time, money, and energy to pursue other long-term goals like starting a business, furthering your education, or extensive travel.

- No Market Volatility: You are not exposed to the ups and downs of the property market.

Making Your Decision: A Step-by-Step Guide

Deciding between Renting vs Buying is a personal journey, but you don't have to navigate it blindly. Here’s a guide to help you make an informed choice:

- Assess Your Financial Health Thoroughly:

- Savings: How much do you have for a down payment, legal fees, and other upfront costs (for buying)? How much do you have for a security deposit (for renting)?

- Income Stability: Is your job secure? Do you expect consistent income growth? Lenders look for stability.

- Debt-to-Income Ratio: How much of your monthly income goes towards existing debts (car loans, credit cards, student loans)? A high ratio can make getting a mortgage difficult.

- Emergency Fund: Do you have at least 3-6 months' worth of living expenses saved up for unexpected events, regardless of whether you rent or buy?

- Credit Score: A good credit score is vital for securing a favorable mortgage interest rate.

- Define Your Lifestyle Needs and Future Plans:

- Mobility: How likely are you to move in the next 5-7 years? If high, renting offers more freedom.

- Family Plans: Do you plan to get married, have children, or live with extended family? This impacts the size and type of property you’ll need.

- Personalization: How important is it for you to customize your living space?

- Responsibility Tolerance: Are you prepared for the responsibilities and potential headaches of property maintenance?

- Desired Location: Do you need to live in a specific area close to work or family? Consider if that area is more affordable to rent or buy.

- Consider the Malaysian Market Trends:

- Property Prices: Are property prices in your desired area rising, stable, or falling?

- Rental Yields: What are the average rental yields in the area? This is crucial if you're considering buying to rent out.

- Interest Rates: Mortgage interest rates can significantly impact your monthly payments and total cost of ownership. Keep an eye on Bank Negara Malaysia's policies.

- Economic Outlook: A strong economy generally supports property appreciation, but a downturn can increase risks.

- Seek Professional Advice:

- Financial Advisors: A qualified financial planner can help you analyze your complete financial picture and model the rent vs. buy scenarios based on your specific numbers and goals. They can also advise on alternative investment strategies if you choose to rent.

- Mortgage Specialists: If buying, they can help you understand your borrowing capacity, different loan products, and current interest rates.

- Property Professionals: Look at available properties and market prices. While we've discussed several excellent sources for information, when it comes to actively searching for properties, platforms like Property Guru are invaluable for exploring listings and understanding current market availability. They can help you visualize what your money can get you, whether you’re looking to rent or buy.

The Final Word: Your Future, Your Choice

The decision between Renting vs Buying is not a race to be won, but a personal journey to be carefully considered. There's no single right answer for everyone. What’s best for your friend, family member, or colleague might not be what's best for you.

For some, the dream of homeownership, the stability it offers, and the potential for wealth creation make buying the clear choice, despite the significant financial commitment and responsibilities. For others, the flexibility of renting, the freedom from maintenance worries, and the ability to invest capital elsewhere offer a more attractive path.

The key is to equip yourself with knowledge, analyze your personal circumstances with brutal honesty, and project your life five, ten, or even twenty years down the line. By meticulously weighing the financial implications, lifestyle preferences, and long-term goals, you can make a decision that truly aligns with your aspirations and sets you on a confident path towards your future in Malaysia. So, take a deep breath, do your homework, and choose the path that empowers you most!

This guide breaks down property investment, homeownership & renting pros/cons in Malaysia.

If you're still feeling confused about whether to rent or buy, take a look at our previous guide to help you make a smart financial move with Making a choice between renting and buying a property involves evaluating various financial factors, lifestyle preferences, and long-term aspirations. Financial institutions often provide comparative guides to help individuals understand the complex considerations for housing decisions.

Frequently Asked Questions

Question: What are the primary factors to consider when deciding between renting and buying a property in Malaysia?

Answer: The decision hinges on several key aspects including your current financial health (savings, income stability, debt), lifestyle preferences (mobility, desire for customization), and long-term goals (wealth building, investment flexibility).

Question: Why is "opportunity cost" an important financial consideration for property buyers?

Answer: Opportunity cost refers to the potential returns you miss out on by tying up a large sum of capital (like a down payment and other buying costs) in a property, instead of investing that money elsewhere, such as in stocks or other ventures.

Question: Are there any hidden costs associated with homeownership that potential buyers often overlook?

Answer: Yes, beyond the monthly mortgage, hidden costs can include maintenance fees (for condos), annual property taxes, home insurance, and unexpected expenses for upkeep and repairs, as well as significant one-off legal fees and stamp duty.

Disclaimer: The information is provided for general information only. JYMS Properties makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.